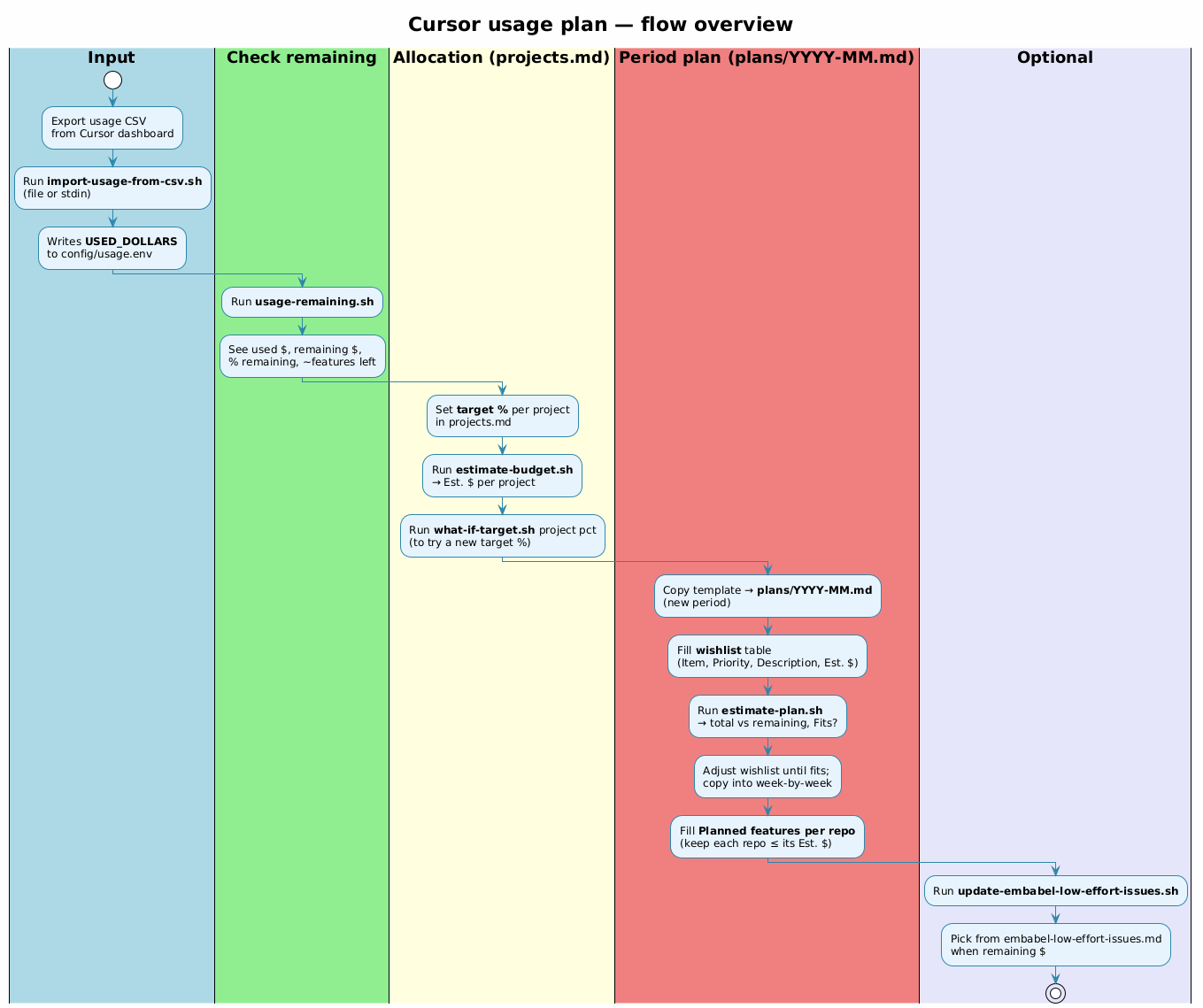

Five phases: Input → Check → Allocate → Plan → Optional

Cursor Ultra gives you a fixed $400 budget each billing period. It resets on a specific day (the 17th in my case)—use it or lose it. Without tracking, you either burn through it early or leave budget unused.

I built cursor_usage_plan—shell scripts and markdown templates to plan usage across projects. It's a template repo: clone it, configure your projects, adapt the scripts.

The Two-Document Workflow

| projects.md | plans/YYYY-MM.md | |

|---|---|---|

| Purpose | Allocation: target % per project | This period's wishlist + schedule |

| Scripts | estimate-budget.sh |

estimate-plan.sh |

The Five Phases

Phase 1: Input

Export usage CSV from Cursor dashboard, then:

Export usage CSV from Cursor dashboard, then:

./scripts/import-usage-from-csv.sh export.csv

Writes USED_DOLLARS to config/usage.env.

Phase 2: Check

See what's left:

See what's left:

./scripts/usage-remaining.sh

Shows: used $, remaining $, % left, ~features remaining.

Phase 3: Allocate

Set target % in

Set target % in

projects.md, then:./scripts/estimate-budget.sh

Keep 10–15% unassigned as buffer.

Phase 4: Plan

Create monthly plan with wishlist (P0/P1/P2 priorities):

Create monthly plan with wishlist (P0/P1/P2 priorities):

./scripts/estimate-plan.sh plans/2026-02.md

Output: "Fits in $400: Yes/No". Drop P2 items until it fits.

Phase 5: Optional

Budget expires on reset day. Use leftover $:

Budget expires on reset day. Use leftover $:

./scripts/update-embabel-low-effort-issues.sh

Note: Embabel scripts are examples—adapt for your projects.

Configuration

MONTHLY_BUDGET_DOLLARS=400

BUDGET_ROLLOVER_DAY=17

DOLLARS_PER_FEATURE=20

Tips

- Plan in $ — Estimate each feature to sum to ~$400

- Check weekly — Run

usage-remaining.sh; if high, add work - Keep buffer — Reserve 10–15% for ad-hoc

- End-of-period — Burn remaining $ before reset